SA-CCR · BIS CRE52 · EBA CRR2

SA-CCR from trade

to capital charge.

Advanced SA-CCR calculator addressing the hardest challenges of the regulation — complex pay-off replication, dynamic asset class attribution, and pre-trade capital impact directly from your front-office system.

Core Coverage

Full coverage of the regulation — no shortcuts

Tested line-by-line against BIS CRE52 (former BCBS279) and EBA RTS-2019-02 as part of CRR2. All intermediate metrics are accessible for auditability.

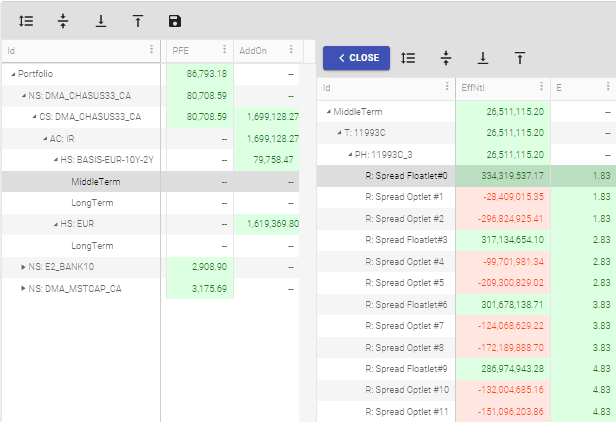

Pay-off Decomposition & Auditability

Complex and exotic payoffs — barrier options, spread products, multi-legged structures — are decomposed on the fly into European options using supervisory volatilities. Every intermediate metric is visible down to the optlet level, enabling audit trails.

Replacement Cost

- Input or computed by Everix

- Netting & collateral set dependencies

- Comprehensive CSA representation

Dynamic Asset Class Allocation

Hybrid products are classified dynamically using FRTB-like sensitivities and risk weights, following EBA recommendations. Example: a Libor FX Spread Barrier is classified as FX, IR, or both depending on moneyness.

- FRTB-like sensitivities for hybrid products

- EBA asset class allocation rules

- Re-classification on market moves

Tailored Integration

Three ways to connect. One outcome.

Use Everix as a complete SA-CCR platform or as a modular engine extending your existing risk ecosystem. Choose the integration depth that fits your architecture.

Full Compute

Everix handles everything

Provide raw deals and market data. Everix runs the full pipeline: ETL, asset class classification, delta computation, PFE simulation, and RC calculation.

- Raw trades + market data as input

- Everix classifies and prices

- Audit trail to optlet level

- Output: RWA, RC, PFE, EAD, AddOn

Your Sensitivities

Bring your deltas

Your system provides pre-computed sensitivities. Everix applies FRTB-like classification rules to assign asset classes and computes the regulatory capital.

- Provide FRTB-like sensitivities

- Everix classifies asset classes

- Handles hybrid/cross-asset products

- Reuse existing front-office analytics

Full Data

Maximum control

Provide both classification and sensitivities from your own systems. Everix applies the regulatory formula, aggregates, and outputs capital metrics.

- Bring your own classification

- Provide sensitivities directly

- Everix aggregates and computes

- Minimal footprint, maximum flexibility

Advanced Features

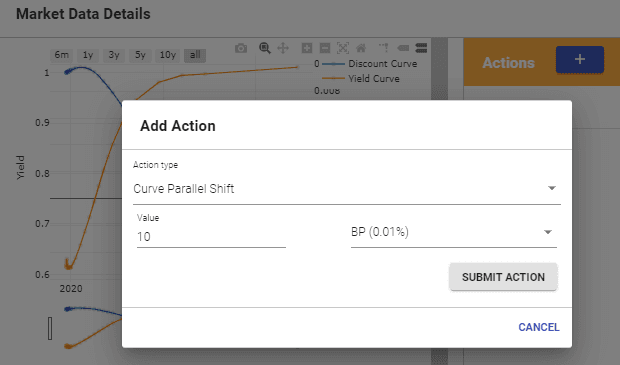

What-If Analysis

- Pre-trade incremental impact

- Market data bumps (curve shifts, surface)

- Trade-level add/remove/modify

- Run via UI or REST API

Marginal SA-CCR

Each trade's marginal contribution to portfolio PFE and Replacement Cost — computed and visible at deal and leg level. Use for charge attribution, limit management, and netting set optimisation.

- PFE reallocation per trade

- RC reallocation per trade

- Drill down to deal & leg level

- Netting set contribution view

SA-CCR Forward

Project your SA-CCR capital cost over the lifetime of the portfolio. Forward RC and PFE are calculated using market data diffusion — giving you a full cost-of-capital curve over time.

- Forward RC based on diffusion

- Forward PFE over trade lifecycle

- Lifetime capital cost forecast

- Integrate into funding cost analysis

Consolidated Risk

All Everix modules.

One portfolio view.

SA-CCR exposure sits alongside XVA, Initial Margin, market risk, and regulatory capital — all computed on the same portfolio. Collateral posted under each CSA is accounted for, so EAD and RWA figures reflect your actual net position.

Related modules

XVA

CVA, DVA, FVA, MVA, KVA — full Monte Carlo XVA with automatic attribution and what-if analysis.

ExploreISDA SIMM™

ISDA-certified Initial Margin calculator with backtesting, IM forward, and what-if analysis.

ExploreIFR / IFD

EU/UK capital requirements for investment firms — K-factors, own funds, and regulatory reporting.

ExploreGet Started

See SA-CCR on your portfolio.

We'll run a demo on a real use case, show you the auditability and pre-trade features, and tell you honestly which integration option fits your stack.